Plastic Restrictions in 30+ Countries Fuel Molded Fiber Packaging Demand

Molded Fiber Packaging Market Size

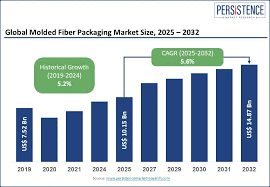

Global molded fiber packaging market projected to grow at ~5.6% CAGR, reaching nearly US$14.87 billion by 2032.

LONDON,, UNITED KINGDOM, January 15, 2026 /EINPresswire.com/ -- The global molded fiber packaging market is gaining sustained attention from investors, manufacturers, and supply-chain stakeholders as sustainability-driven regulations converge with improving cost structures and stable end-use demand. Molded fiber packaging—also referred to as molded pulp packaging or fiber-based packaging—is increasingly positioned as a structural replacement for plastic and foam packaging across foodservice, consumer goods, and protective packaging applications.

The global Molded Fiber Packaging market is rapidly transforming the sustainable packaging landscape as eco-friendly alternatives to conventional plastics gain unprecedented traction. According to the latest industry forecasts, the molded fiber packaging industry is projected to grow from approximately US$10.15 billion in 2025 to US$14.87 billion by 2032, recording a steady CAGR of around 5.6% between 2025 and 2032.

This surge is driven by increasing demand from food & beverage sectors, consumer electronics, and healthcare & medical packaging applications, underscoring the role of molded fiber packaging as a biodegradable and recyclable solution for global supply chains.

Download Your Free Sample: https://www.persistencemarketresearch.com/samples/35499

Recent Market Trends

Key molded fiber packaging trends shaping the global market include:

Rise of Dry-Molded Fiber Technologies — Automated dry molding systems (e.g., PulPac’s dry molded fiber machines) reduce water use by up to 95% and increase line speeds, making sustainable packaging competitive with traditional plastics.

Shift to PFAS-Free and Barrier Coatings — Development of compostable and moisture-resistant molded fiber coatings supports foodservice and hospitality industries aiming to eliminate plastic liners.

Mounting Foodservice Demand — Custom molded pulp trays and clamshells are increasingly replacing single-use foam and plastic solutions in quick-service restaurants and grocery retail.

E-Commerce Protective Solutions — Precision-engineered molded fiber inserts for packaging electronics and fragile goods offer shock absorption and sustainable credentials for online retailers.

Agro-Waste and Non-Wood Pulp Adoption — Brands are shifting to sugarcane bagasse, wheat straw, and other non-wood pulps to strengthen sustainability positioning and reduce cost volatility.

These compiled molded pulp packaging insights signal a broader transition toward packaging solutions that are ecologically responsible yet commercially viable — resonating with sustainability-driven consumer behavior.

Why Investment Interest Is Increasing

Investor interest in the molded fiber packaging market is primarily driven by structural market certainty rather than short-term growth speculation.

First, sustainability requirements have transitioned from voluntary initiatives to enforceable regulations. Molded fiber packaging directly aligns with circular economy goals, reducing long-term compliance risk for manufacturers and investors.

Second, production economics are improving. Automation, higher mold precision, and material efficiency are lowering per-unit costs, narrowing the historical price gap between molded fiber and plastic packaging. As capacity utilization improves, operating margins are becoming more predictable.

Third, demand is concentrated in essential, high-volume end-use industries such as food packaging, egg cartons, foodservice disposables, and protective industrial packaging. These applications exhibit lower demand volatility, even during economic slowdowns.

Finally, multinational brand commitments to recyclable and compostable packaging formats are creating long-term supply agreements. Once packaging systems are redesigned around molded fiber formats, switching costs increase, enhancing revenue visibility and supplier stability.

Customize This Report to Your Needs: https://www.persistencemarketresearch.com/request-customization/35499

Segment Analysis

The global molded fiber packaging market segmentation reveals nuanced demand patterns across product types, molded techniques, and end-use industries:

1. By Product Type:

Trays dominate the structured packaging landscape — widely used for egg cartons, fruit trays, and consumer food products due to their lightweight, protective, and eco-friendly properties.

Clamshells & Containers are gaining ground, especially in foodservice and retail sectors looking to eliminate single-use foam packaging.

2. By Molded Type:

Transfer-molded fiber packaging remains the backbone of the industry due to cost efficiency and established automation.

Thermoformed and Dry-Molded Fiber segments are rapidly expanding, especially where high-precision and premium finishes are critical — such as in consumer electronics inserts and cosmetics packaging.

3. By End-Use:

Food & Beverage continues as the largest end-use category, propelled by regulatory bans on plastic and the growing shift toward biodegradable molded fiber solutions.

Healthcare & Pharmaceuticals and industrial packaging are emerging segments where stringent quality and sustainability standards are influencing purchasing decisions.

This detailed segment analysis highlights how the molded fiber packaging market is broadening beyond conventional uses, emphasizing value-added, performance-oriented niches.

Regional Analysis

Geographic expansion in the global molded fiber packaging market is not uniform but marked by strategic growth pockets:

Asia-Pacific leads by revenue share, accounting for over 40% of the global market due to the booming foodservice, e-commerce, and FMCG sectors — with China and India driving adoption.

North America remains a key market, supported by plastic reduction mandates and retailer commitments to sustainable packaging solutions.

Europe shows strong momentum with circularity regulations such as the EU’s Packaging and Packaging Waste Regulation enhancing demand for fiber-based packaging.

Emerging markets in Latin America and the Middle East & Africa also present incremental opportunities, particularly where plastic bans and sustainable policies intersect with rising consumer demand.

Buy Now for Actionable Intelligence: https://www.persistencemarketresearch.com/checkout/35499

Industry Players

The competitive landscape of global molded fiber packaging is defined by established multinational players and innovative disruptors:

Huhtamaki Oyj: A global leader investing in dry-molding technology and sustainable foodservice packaging.

Brødrene Hartmann A/S: Dominates egg packaging and precision-molded fiber solutions in Europe and Latin America.

Pactiv Evergreen Inc. & Genpak LLC: Focused on PFAS-free fiber containers for food retail and QSR chains.

PulPac AB & Zume Inc.: Pioneering automated dry-molded fiber production and advanced compostable coatings.

CKF Inc., Fabri-Kal, UFP Technologies, and EnviroPAK Corporation: Regional innovators expanding portfolios with customized molded fiber solutions.

These industry players are intensifying competition through strategic partnerships, capacity expansions, and product innovations that appeal to global sustainability goals and commercial performance standards.

Persistence Market Research

Persistence Market Research Pvt Ltd

+1 646-878-6329

email us here

Visit us on social media:

LinkedIn

X

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.